A note on Glencore

Coal mergers, a drop in margins, cyclicality and China... what's the deal with Glencore right now?

The A.I. rush is still going — but for how long?

And how will that affect equity markets at large as Apple and Google have slowed down considerably? I explore the broader market setup in a piece which you should not miss, linked below.

The piece includes a long analysis on the AI-theme and whether it’s a Sorosian boom/bust (i.e. Reflexive Bubble) or not. The piece is behind a paywall ($).

Philoinvestor

Philoinvestor

I warmed up writing the Reflexive Bubble piece with this free-for-all piece below that has >100,000 views on Twitter as of now.

Philoinvestor

The Setup on Glencore

2022 was a blowout year for Glencore — EBIT reported was almost 3X higher than in 2021. The post-Covid paradigm and the war in Ukraine layered on top, caused havoc in energy markets.

The market saw price spikes in oil, gas and coal — and Glencore happens to have a lot of coal. From the bottom of the March 2020 low, to the peak of November 2022 Glencore returned a 4.5X and paid some dividends along the way too. But now what?

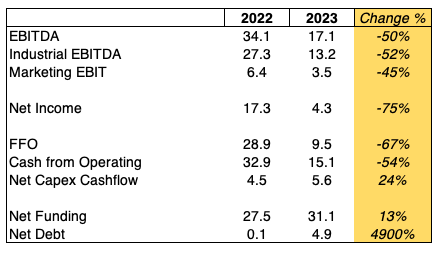

How was 2023?

*Figures are adjusted, always look at official company financials to verify.

Ok so, by and large 2023 was half the year 2022 was. Glencore puts the drop in performance on a return to a “normal backdrop” in trading conditions, which resulted in the Marketing segment slashing its Adj. EBIT figure by 45%.

Further to that, energy commodities and metals prices normalised (i.e. tanked), halving Adj. EBITDA in the Industrial segment as well. Note that $13bln of that EBITDA drop was driven by price reductions alone.

With a halving in EBITDA, net income dropped by 75%, because of operating deleverage.. (obviously)

The point is, 2022 was a blowout year and Glencore’s financials have now reverted to a more normal environment. But “normal” doesn’t really exist in commodities and energy, coal prices could tank from here and cause problems for Glencore.

How do I know coal prices will remain elevated? (rhetorical question)

Glencore Trading

This slide carve-out below illustrates what a blowout year their Marketing (i.e. trading) segment had in 2022, and how it quickly snapped back to the mean in 2023.

While Metals & Minerals remained level year on year, Energy Products EBIT (referring to Marketing here) dropped from a massive 5.2bln to 1.7bln. Now with the disruptions in the Red Sea, and the Houthis undeterred, it’s hard to gauge what their trading can achieve next year.

In the last earnings call, I feel that the CEO dodged the question when asked:

“I mean I don't like to think about it that way because obviously, our biggest concern is about the well-being of any vessels and the crew on any vessels that we have on the water. Naturally, as a byproduct of some sort of geopolitical tension that does create opportunities. I don't sit here and try and identify and say, yes, we made a whole lot of money out of these things. But our main concern is that there has been disruptions, there has been issues. There has been diversions. You've got more sailing rates, you've got higher freights in certain categories of freight, not really dry bulk, but more container. And that has created certain arbitrage opportunities, which we have capitalized on, but that's not something that I pay that much attention for. I'm more concerned that through these disruptions, our assets and our people are safe.”

Management has long-term guidance for the Marketing segment of between $2.2 and $3.2 bln in Adj. EBIT per year. That’s a pretty wide range, natural to this kind of business, and confirming my view that one must apply a wide margin of safety when investing in this company…

Glencore Industrial (Metals, Minerals and Energy)

The delta in performance in Industrial was similar to their trading segment. The carve-out illustrates the goings on.

Of the $14bln drop in EBITDA (shown above), $10bln was from Coal mining. The rest was from metals and to a lesser extent oil & gas. The drop in metals prices compressed margins y/y and resulted in lower profits. In the case of Nickel, margins went slightly negative (note: this can happen in cyclical industries!).

The drop in coal prices took margins from a crazy 65% to a still-great 48%.

The Coal Spinoff

Glencore was in a conundrum. They had to become more ESG, while at the same time still ride the trends they deemed to be the most profitable. Glencore management seems to believe in the coal business — and that’s why they pursued Teck’s coal division (i.e. EVR, Elk Valley Resources).

Late last year they closed a deal to snatch 77% of that division for $6.9bln. They signalled at the same time that they would be spinning off the totality of their coal assets (EVR + their existing coal assets).

But they said the spin off would happen in two years, and only after they merge their own coal assets with EVR’s steelmaking coal assets.

Note that the transaction is expected to finally close in Q3 of 2024, after authorities and regulators sign off (or not).

For reference, the combined coal assets (Glencore + Teck’s EVR) are expected to generate $7.5bln for 2024. Last year Glencore made $8bln on its coal assets alone.

Management has signalled in earning calls that the eventual decision to spinoff or not, will be decided by shareholders. Management themselves intend to spinoff but that finally rests on shareholder approval.

Capital Return and the Balance Sheet

Glencore has been managing their “Net debt cap” at the $10bln level. Now with the EVR expected to close late this year, they have revised that to $5bln.

They just want to keep a lower debt level and further robustify their balance sheet. But to do that, considering the money they will pay for the EVR acquisition, they need to “deleverage” a bit — $8.4bln of deleveraging required to hit the $5bln net debt target.

To achieve this they had to modify their shareholder returns framework — the base case now predicts dividends of $0.13 per share (with top ups as the balance sheet allows).

Conclusion

The company is selling right now for a market cap of 47.1bln Pounds Sterling on the LSE, that converts to roughly $60bln. The company generated $4.3bln in net income for 2023, and $17bln in 2022.

For a commodity-related capital-intensive cyclical company, that buys back shares at any price, while China is slowing down and the EV theme is facing a wall (I believe) — one needs to be very careful about the prices he chooses to pay.

As you can understand, valuing this complicated business is extremely difficult. But in life and in investing — what matters is operational success. To make money from this company, one needs to buy at deep discounts (the margin of safety).

For me, we are not there yet.

Sincerely,

Philo