Apple's Microsoft moment.

Sherman Act Case against Apple increasingly possible. EU already pushing.

Most of you have heard of the famous United States v. Microsoft Corporation case where the latter accused Microsoft of illegally maintaining a monopoly in the Personal Computer (PC) market — and engaged in “tying in” violations as per the Sherman Antitrust Act.

Judge Jackson issued his findings of fact on November 5, 1999, holding that Microsoft's dominance of the x86-based personal computer operating systems market constituted a monopoly, and that Microsoft had taken actions to crush threats to that monopoly, including applications from Apple, Java, Netscape, Lotus Software, RealNetworks, Linux, and others. On April 3, 2000, Jackson issued his conclusions of law, holding that Microsoft had committed monopolization, attempted monopolization, and tying in violation of Sections 1 and 2 of the Sherman Antitrust Act.

On June 7, 2000, the District Court ordered a breakup of Microsoft as its remedy. According to that judgment, Microsoft would have to be split into two separate units, one to produce the operating system and one to produce other software components. Microsoft immediately appealed the judgment to the D.C. Circuit Court of Appeals.

Us Vs Microsoft, Wikipedia Article.

Does Apple reap monopolistic advantages?

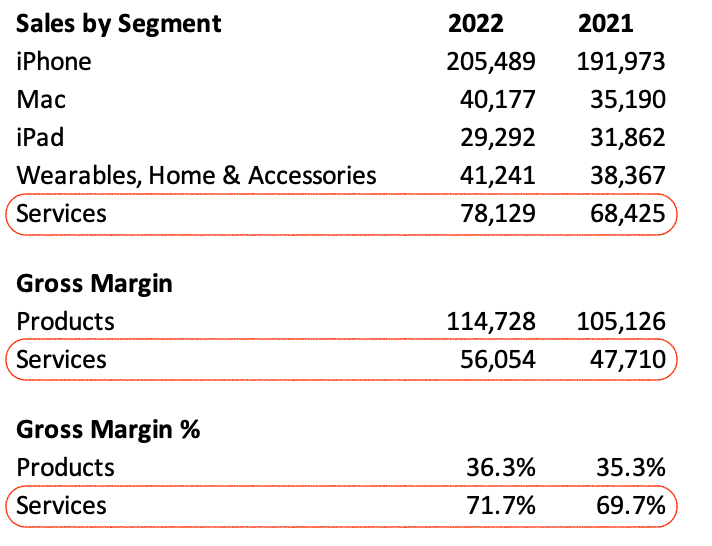

Besides the obvious iPhone, Mac, iPad and peripheral sales that Apple makes a profit from — the company also achieves sales of ~$78bln in Services. In my opinion, all the lines under Services are in risk of being targeted in the US DoJ brewing antitrust case against Apple. Why?

Well, all line items under Services benefit (unfairly) from the Apple ecosystem.

A tying arrangement you say?

Under Section 1 of the Sherman Act, in simple terms a tying arrangement is when the sale of a product conditions the sale of another product when the arrangement strongly hinders free competition and the seller has significant market power. When these conditions are met, that’s illegal! This guy knows that well… 👇

So, it’s debatable that Apple would not be in such a well-placed competitive (monopoly basically) position if it didn’t exert absolute influence of its ecosystem. Just because the Apple ecosystem runs on Apple devices does not mean that only Apple can/should sell Cloud services, place Apple software in (absolutely) advantageous positions, disallow 3rd party app stores and generally lock the ecosystem so they only can benefit from it financially.

This is basically what the pending antitrust case will argue.

Valuation?

Apple is 12.5% of the Nasdaq 100, that’s a very heavy weight. Apple’s price rally, and generally the unstoppable Big Tech rally, have carried the Nasdaq to ever-greater heights. It’s been nice for passive investors all around.. 🤑

Last year in the Rufus: Quest for the Safe Stock piece I argued that “safe stocks” do not exist, and gave examples of that vis-á-vis the darlings of the stock market — i.e. Big Tech. I advise all of you to read and study that essay, if you are serious about your investing.

Apple is currently selling for ~30x earnings and is still basically the best company in the world. But a lot of its tailwinds are now turning into headwinds, and valuation is really on the high side. Do you expect the stock to perform as it did in the past?

🇨🇳🇨🇳🇨🇳🇨🇳🇨🇳🇨🇳

On top of the Sherman Act antitrust case which could hurt its sales and bottom line — geopolitical developments and escalating protectionist measures between US and China could see sales in Greater China get hurt too. For 2022, Apple made ~$30bln in EBIT from Greater China alone.

🇪🇺🇪🇺🇪🇺🇪🇺🇪🇺🇪🇺

If that wasn’t enough, the EU is cornering Apple as well. EU rules being applied on phones being sold starting in 2024 require Apple to dump the lightning port and go with standardised USB-C ports on all its devices.

Past performance is not indicative of future results. Make sure to know your stocks better than most.