Farfetch to 10X?

Misunderstood as just a marketplace...but actually the technology stack for the global fashion industry.

Farfetch is the creation of José Neves, a Portuguese self-proclaimed geek who launched a tech company at the age of 19 before moving to London and opening his own boutique.

In 2008 by marrying technology with fashion, he launched Farfetch. His vision was to create a portal for independent boutiques to compete with the leaders of fashion e-commerce.

The inspiration for the idea came to him in 2007. He realised that small boutiques around the world would go out of business because the internet would change the industry. José realised that they were NGMI, and fashion would become poorer for it.

Today Farfetch is undoubtedly a force to be reckoned with in the luxury industry. But how did José achieve this in a space which was so reluctant to jump online?

Using the Wedge 🧀

José used the wedge, as explained by Lenny Rachitsky on his Substack.

José didn’t go to Gucci, Fendi or Prada and ask them to join the platform, because chances were he would fail abysmally. No, what he did was much smarter. He went to independent boutiques, possibly ones that already knew him personally, and convinced them to join.

Using the wedge strategy, Farfetch launched as an e-commerce marketplace for luxury boutiques. Farfetch launched with 25 boutiques selling a total of 500 brands.

Today Farfetch connects customers with items from over 1,300 of the world’s best brands, boutiques and department stores.

The Farfetch Marketplace

Unlike Net-A-Porter, the online luxury business founded by Natalie Massenet in 2000; Farfetch holds no inventory. Net-A-Porter is a 1P marketplace, Farfetch is a 3P marketplace. What’s that?

A first-party relationship (1P) means the marketplace acts as the retailer, and the brand is the wholesale supplier. A third-party relationship (3P) is when the brand is the retailer, and sells directly to buyers via the marketplace.

As of Q3 2021, the marketplace has 3.6 million active customers up 31% y/y.

The pandemic was a tailwind in attracting new customers as it only had 2.1 million at y/e 2019. (It grew 50% from y/e 2018)

The marketplace can be accessed at Farfetch.com or via the Farfetch app, and it allows vetted sellers to sell their items globally to Farfetch customers.

Farfetch (FF) gets a “take rate” of 25-33% from each transaction. Of course that doesn’t come easy as FF has to spend money on technology, demand generation, general & administration expenses, logistics etc., to keep the marketplace up and running.

At the moment the company is focusing on gaining market share and becoming the leader, which causes net margins to be compressed due to the investment required to ramp up the business.

As the marketplace scales over time and the fixed cost base is levered further, the true business economics of the company will show.

“Sometimes value creation cannot be captured by accounting considerations or value-dogmatic preconceived notions. Sometimes value creation is a positive on a balance sheet, sometimes it’s a negative on the income statement. Sometimes it is nowhere to be found. But just because you can’t see it on a financial statement, doesn’t mean it’s not there.”

-Philoinvestor

Besides the Farfetch.com marketplace, the company also runs Stadium Goods, a marketplace specialised in the resale of sneakers. Stadium Goods operates physical stores as well as an online website. FF spent $250 million to acquire Stadium Goods and believes strongly in this segment.

This acquisition signals FF’s ambitions of growing in the premium sportswear market. The future opportunity is encapsulated below:

“The deal expands Farfetch beyond a marketplace for retailers to sell designer goods, as Stadium Goods is a marketplace for individual resellers,” Matt Powell, senior sports industry advisor at The NPD Group. “By using the Stadium Goods platform, Farfetch can expand into other peer-to-peer categories, while Stadium Goods will benefit from having a greater capitalization.”

Not just a Marketplace

In 2019, FF acquired New Guards Group (NGG) and created its Brand Platform.

This move not only places a number of high caliber and growing luxury brands (Off White, Palm Angels etc.) under the FF umbrella, but also gives the company the capacity to create new brands internally.

The acquisition adds a “Brand Platform” layer to Farfetch’s existing Technology, Data and Logistics Platform layers, extending capabilities beyond technology solutions and global distribution into design, production and brand development. Link.

When this acquisition was announced in August of 2019, the FF share price gapped down to a 45% loss closing at $10 per share. Investors did not seem to like this pivot by Farfetch. They thought, “Why would an aggregator platform start to compete with its own sellers? Why spend $675 million when you are not even profitable to acquire brands?”

But José Neves, the visionary behind Farfetch offers his own take.

I do understand the reaction and the questions. I think the first thing to realise is, “What is NGG?” and the way I see it…they are a platform and they were so even before they started talking to Farfetch. They see themselves as a platform, they have a common infrastructure in terms of design, sales, marketing, showrooms, same industrial platform team.

José goes on to explain the idea that Farfetch must become like a Netflix or a Spotify:

For me, it’s like they are Pixar - and yes they have Toy Story, and Monsters Inc. and now they are on to the next one. To me it’s really about original content, and this idea that I really firmly believe in. The idea is that consumer-facing platforms, such as Farfetch, need to have an element of original content. And I think the best analogy is Netflix - so Netflix started aggregating an industry and there was an inflection point when they said: “If we continue to be just an aggregator of content that everyone else has, this is going to be difficult in terms of margins, customer acquisition, building a brand..” and obviously that inflection point was very brave, no one liked it, it consumes much more capital…but it created the $100 billion plus company that we know today. I don’t think they would be around if they were just a standardised platform.

José also talked about Spotify when it had to pivot to create its own content. Spotify spent billions investing in podcasts. Spotify was already killing it and winning against Apple. And everyone was wondering why they did that. And the answer is that Spotify had to differentiate.

Consumer brands that start as aggregator platforms move to become partially as creators of content themselves. And that is the way we see NGG.

The Farfetch Platform

Ever since the early days when Jose was visiting boutiques and trying to convince them to join the marketplace, a pattern was emerging. Some of them did not want to join the marketplace at the time, but were still sold on the idea of going online. They asked Jose to help them create their own website.

And Farfetch Platform Solutions (FPS) was born, you can think of it as a white label technology offering.

“Use our full suite of solutions to create a new website, app or digital experience, complete with payments, an order management system, global logistics, stock optimisation and content management systems.”

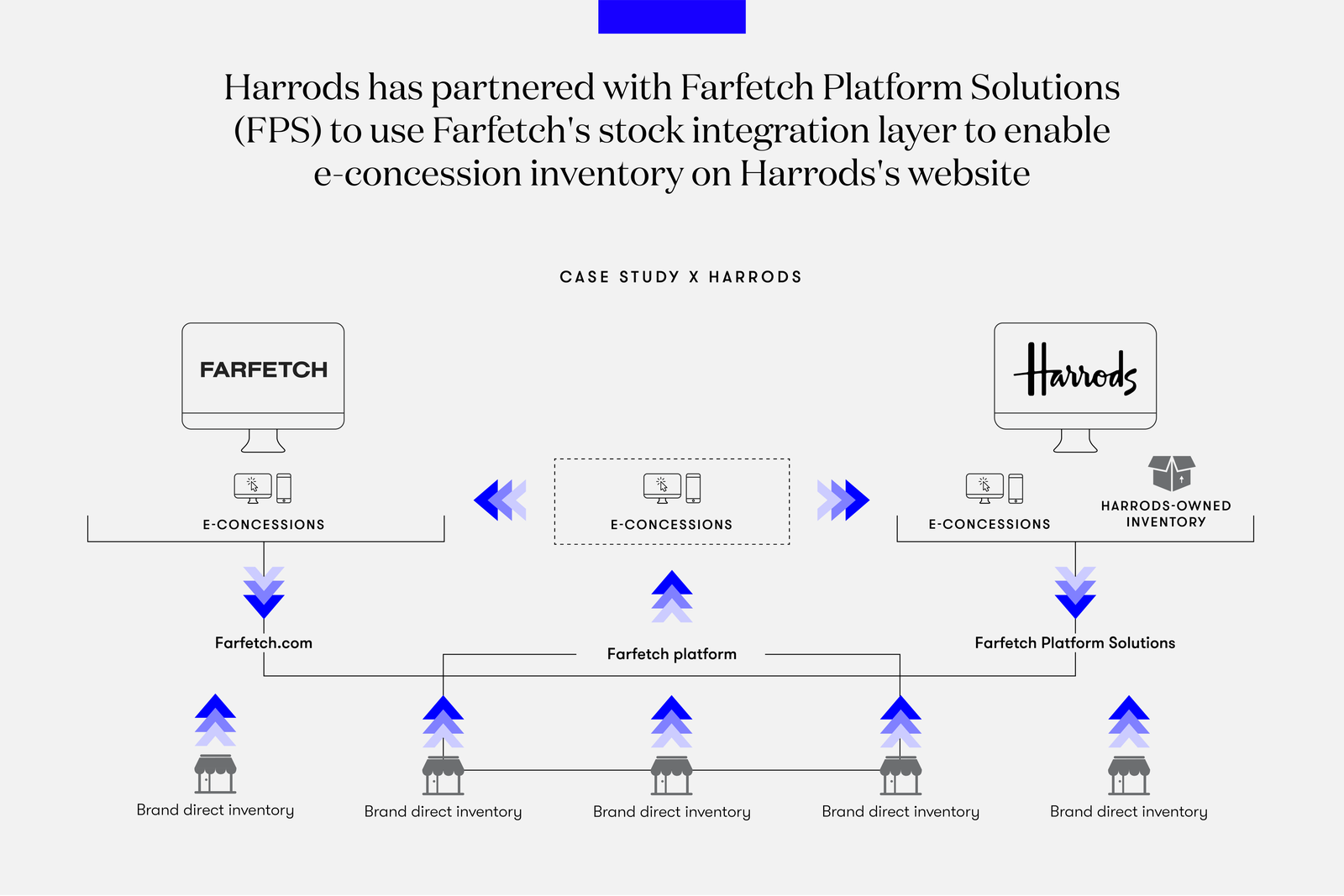

e-Concessions

With this system, FF connects to a brand or department store and knows in real-time the stock of inventory that exists at any place in their storage infrastructure. For example, with Prada Farfetch has 70 integrations.

Farfetch is now pushing what it calls e-concessions as a service. This means that Farfetch can handle the sales of a brand made through a multi-brand department store’s website. The department store doesn’t need to buy or hold inventory (as in a traditional wholesale relationship), as Farfetch directly plugs in to brand stock systems. E-concessions enable multi-brand retailers to offer a greater assortment of a brand’s inventory, as it can list the same products across multiple sites from the same bucket of inventory. José calls this infinite shelves.

Why is Farfetch doing all this? Where are they going?

We platformize everything we do, so people can use every element of the Farfetch infrastructure. They can use order fulfillment, they can use our multiple payments systems all over the world, they can use our e-concessions.”

We invented the e-concessions model and now we are bringing it as-a-service. Why don’t we platformize it? Let’s open it so that other retailers like Harrods can use it. Harrods now has 3 concessions and counting with spectacular explosion of sales for these brands once they move to an e-concessions model. I think this becomes an even more powerful mission.”

“Fast forward in 10 years we really want to service the top brands and top retailers in the world, with every single need they have in terms of retail. That is why we call it luxury new retail: Online, offline, monobrand, multi-brand etc.

Distributed Logistics & Fulfillment by Farfetch (FBF)

Farfetch has invested in its own distributed logistics model with 6 global warehouses where sellers can consign the merchandise and FF can ship them to the buyer directly. This saves costs and time making the customer experience much better.

Only a small percentage of sales go through FBF and José has stated that the bottom line will be positively affected as this increases over time. Besides these 6 third-party owned global warehouses that FF operates, they run a distributed logistics model with more than 1,000 inventory points globally.

The investment in infrastructure and technology that FF has allocated to their logistics model allows for same-day delivery in 19 major cities and super-fast delivery in almost all other cities in the world.

Farfetch China / Alibaba and Richemont

On November 5th, 2020, Farfetch announced a major strategic partnership.

“Farfetch, Alibaba Group and Richemont form global partnership to accelerate the digitization of the luxury industry.” On to the important bits of this partnership:

- Alibaba launching a Farfetch sales channel on its own marketplaces, the Tmall Luxury Pavilion (TLP) and Luxury Soho.

- Richemont will also explore additional opportunities to work closely with Farfetch in a number of initiatives.

- Both Alibaba and Richemont to invest in both Farfetch Limited and the Farfetch China Joint Venture.

This gives Farfetch a number of strategic advantages in the race to consolidate the global luxury market. Most importantly, access to the Chinese customer via Alibaba’s TLP. Tmall boasts 800 million customers.

This will allow Farfetch sellers to have a seamless integration with the Chinese market. Farfetch launched in early 2021 on TLP with 3,500 brands, of which 90% were new to Tmall.

How did this deal come about? Jose explained that the genesis of the deal was from a conversation that Jose had with Alibaba about the state of the luxury retail market. Alibaba and Farfetch concluded on a common vision to power, empower and enable retail.

Luxury New Retail (LNR)

They decided to join forces to create this vision of Luxury New Retail.

Richemont, the luxury goods conglomerate already had a close relationship with Alibaba and it also agreed to be a part of the LNR initiative. This has sparked the conversation between FF and Richemont to further their partnership in a number of ways. The initiatives listed below are not to be taken lightly.

In this context, Richemont is in advanced discussions with Farfetch with a view to enhancing the partnership it established last year. The scope of the current discussions includes:

(i) Farfetch investing directly in YOOX NET-A-PORTER as a minority shareholder, with other investors to be invited to participate alongside;

(ii) YOOX NET-A-PORTER leveraging Farfetch Platform Solutions to support its ongoing transition to a hybrid 1P/3P business model;

(iii) Richemont Maisons leveraging Farfetch technology to accelerate their Luxury New Retail developments; and

(iv) Richemont Maisons joining the Farfetch marketplace.

The Farfetch China JV

The JV will own the Farfetch China marketplace operations (B2C). The B2B operations (i.e. FPS), will stay under the direct ownership of Farfetch Limited.

Alibaba and Richemont will invest $250 million each in Farfetch China for a 12.5 stake each. They have an option to acquire a remaining 24% after the third year of the venture’s formation, if certain targets are achieved.

Together with this investment in FF China, Alibaba and Richemont will each acquire $300 million of Farfetch Limited 0% convertible senior notes due 2030. The noteholders have the right, at anytime before the 2030 maturity, to convert the notes at a price of $32.29 per share. Considering full conversion, this would add 18.5 million shares to FF’s total outstanding shares.

A Force for Good

The path to the starlit heights of the fashion industry is not exactly paved with roses. We don’t proclaim to have experienced the pain and unfairness of those working in the industry. So we will let James Scully, superstar casting director, do exactly that in this emotional talk.

Why would models, photographers and all types of fashion-related workers be forced to go through such abuse for a job? Maybe it’s because they optimised and focused their whole lives into working for this industry, and they had no alternative.

Then, due to the state of the industry, they found themselves in a position where they had become forced sellers of whatever skill or talent they had.

What does this have to do with Farfetch?

Farfetch is an enabler, not only of existing and incumbent brands to sell online around the world. It is an enabler of new brands, upcoming designers and companies with limited financial resources to create a brand as well as a following and distribute their product without the need for massive financial investment.

This creates alternatives. It creates opportunities for fashion workers to find work outside the grip of those that have abused their power and position in the industry. This creates value. And in business, value creation is profit - especially in platform businesses like Farfetch.

And if that were not all, enter Media Solutions

Farfetch has launched this business line which it believes one day will be 4% of company sales. This is a high margin business.

Brands can use media solutions to market themselves to the Farfetch ecosystem and boost sales. Imagine a new brand just starting out. It has no stores, it has no customers. Marketing on Farfetch would give them exposure to a wide demographic of potential buyers.

This lowers the required financial investment greatly and opens up a word of opportunity.

Rounding it all up

Farfetch is still in its early days. We believe it has decades of growth ahead of it.

To put some numbers in context. Farfetch has a total of 3.6 million customers, while China alone has 30 million luxury shoppers. This is a tremendously low penetration. The luxury space is growing at ~5% per year and expected to grow at those rates for the considerable future.

The TAM for global luxury is at $300 billion, while FF’s yearly GMV was a mere ~$3 billion. Pre-Covid, 12% of luxury sales were transacted online and they have now stabilised at 20%. In 5-7 years time that’s expected to go to ~35%.

FF currently commands 5% of online luxury sales while online leaders (e.g. Booking.com, Spotify) typically command 30-40% market share. Farfetch is still far from those numbers.

Farfetch is not a retailer, nor is it a disruptor. Farfetch is a technology company and a platform. It is consolidating the space and emerging to be the technology stack for the global fashion industry.

Farfetch is currently selling for ~$10 billion. Let’s use a back of the envelope calculation to see if this current valuation is an investment opportunity.

Assuming FF gets to 40% market share of online luxury sales, while the latter doubles to $120 billion, would give Farfetch a GMV of $48 billion. At that figure the current price would mean FF is selling for a Price to Future Sales of 0.2X.

This excludes the Brand Platform, which has ample room to grow with existing brands, newly developed ones and future acquisitions.

Things to look out for in 2022

-The Farfetch Beauty launch on an “only on Farfetch” basis.

-Doubling down on Fulfillment by Farfetch.

-Doubling down on Media Solutions.

Watch this space for updates on our view over time.