George Soros - the basics.

Notes from The Alchemy of Finance etc.

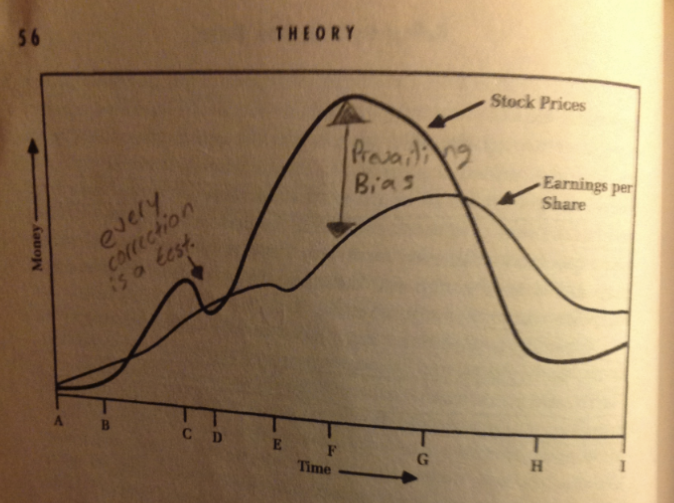

The Theory of Reflexivity

There are two connections at play in the theory of reflexivity, the participating and cognitive functions. The underlying trend influences the participants’ perceptions through the cognitive function; the resulting change in perceptions affects the situation through the participating function.

In the case shown above: we can say that EPS are the fundamentals and the Stock Prices are the perception of the fundamentals, or the perception of reality. The difference between the two is the prevailing bias, however the prevailing bias can influence the EPS and the EPS can in turn affect the Stock Prices. This short circuit can be done in a myriad of ways different in each case. Of course, the model above can be used for cases other than stock prices and EPS.

Far From Equilibrium

The markets are in a state of far from equilibrium conditions when 1) the rules have changed and/or 2) there is a clear reflexive connection happening, causing the markets to be anything but in equilibrium. It is generally a condition when the events run faster than our ability to understand them and that includes the regulators/authorities which sometimes try to intervene in the markets to bring back “equilibrium”.

When the rules change the end results of investment decisions are so much different that all your calculations are way off than previously thought. A recent example is the Soros bet of buying Italian 10-year government bonds, if the markets continued the meltdown the Italian bond would crash in price, if the markets came back from the brink then you would have doubled your initial investment. That is the complexity and the confusion of investment decisions in the markets today.

This happens when the cognitive function and the participative function move in the same direction, causing a self-fulfilling cycle which affects the so-called fundamentals to match the prices and the prices affect the so-called fundamentals. In this case “reality” is altered and things look much different than they were but there is a reality beyond our ability to understand it and sooner or later that catches up with us. In all of these cases there is a flaw in the bubble and you should keep your eyes and ears open for it. You should stay vigilant and be ready to change your mind.

When the seeds have been sown

In his essay, “Does the euro have a future?” George mentions a case where the inability of the authorities to do enough and but merely opt to “kick the can down the road” which in turn sows the seeds for the next crisis.

You have to keep your eyes open for such cases. They provide valuable cues for future occurrences.

On Oil 🛢️

In a testimony dated June 3, 2008 before the US Senate George spoke about the reflexive process of the price of crude oil.

There are four major factors at play which mutually reinforce each other. Two are fundamental and two are “reflexive”. One is peak oil, even though higher prices make it economically feasible to develop more expensive sources of energy. Second, there is a “reflexive” tendency for the supply of oil to fall as the price rises, reversing the normal shape of the supply curve. Therefore, for oil producers who expect the prices to rise further there is less incentive to convert oil reserves underground into dollar reserves aboveground therefore their (flawed) perceptions matter greatly. This has led to what may be described as a backward sloping curve. Third, countries with the fastest growing demand-notably the major oil producers keep domestic energy prices artificially low by providing subsidies and thus price rises do not reduce demand. Finally, demand is reinforced by speculation that tends to reinforce market trends.

To the brink and back macro trades

The euro was a in a “brink and back” phase and this is why there was a free put on that trade. You could reasonable expect something to happen from the authorities that would reverse or at least halt the drop of the euro. However, even the stopping of a euro drop turns on certain dynamics which have an upward effect on it. To spell it out, the euro, by stopping its decline could start its rise.

Referring to market dynamics, the actions of all the agents within the market like accumulation of speculative positions, and most actions that drop the market caused by fear. As the market stabilises these things will reverse.

Bullet Points from The Alchemy of Finance

- There is a paradox when buying in the midst of a trend. You may be caught in the midst of a correction.

- Historical events tend to break historical patterns.

- Temporary solutions are only temporary. They will resurface.

- Oil has an inverted supply curve. As prices drop, supply goes up because producers have to sell more barrels to make the same amount of money to take care of their “responsibilities”.

- The “brink” model is the model that describes the immediate, massive and urgent concerted response from national and international institutions to save the financial system.

- Soros was tentative with his positions when the market was not obliging. Testing his theses, first.

- “The market’s response gave me courage to take on a large exposure.”

- “My perceptions are partial and subject to correction by events”. “Recognising my mistakes is a source of pride”.

- Once we realise the imperfect understanding is the human condition, there is no shame in being wrong, only in failing to correct our mistakes. This is what GS means that he was correcting his mistakes.

- Taking a large market bet is less dangerous than predicting eventual outcome patterns.

- I shall assess the cycle by identifying the “thesis” that the current market rally incorporates.

- Markets tend to be a predictor of the economy, the future, events etc.

- Soros speaks a lot about “tests” when he is assessing his market theses. When a market is in an uptrend or boom phase, and there is a sharp sell-off, Soros considers the sell-off as a test of the overall trend.

The market (thesis) could pass the “test”, and then continue to go higher, which is often the case. Or the market thesis could fail the test and then enter into a new phase, usually a down trend.

Follow the markets in a trial and error way where non-falsification of the hypothesis means things are going well but falsification of the thesis means I have something wrong and I have to fix my mistakes. Soros prospered by being a trader with a highly asymmetric profile. When the market was moving with his thesis and position he was positioned, when it wasn’t, he was out and re-assessing the situation.

The market theses that he was formulating, all had the objective of allowing GS to take trades in the marketplace with operational success in mind. He was never married to his ideas and theses, and financial survivability and success were always the primary objective.

When the market confirmed his theses, by going his way, he would stay on the trade or add to it. When the market was disconfirming his theses, he would cut the position or exit completely.

I learned the hard way that the range of uncertainty is also uncertain and at times it can become practically infinite.

-George Soros