Is Elon flying too close to the sun?

And a small story about Eike Batista's complacency and hubris.

In Greek mythology Icarus was the son of Daedalus, a master craftsman and creator of the Labyrinth. They attempted to escape from Crete using the wings that Daedalus created out of feathers and wax.

In this grand escape, the father warned his son of complacency and hubris. He instructed him to neither fly too low lest the sea’s dampness clogs his wings - nor fly too high lest the sun’s heat melts them. Icarus ignored his father’s advice and flew too close to the sun, causing his wings to melt and resulted in his fall from the sky.

Enter Eike Batista

In 2012, Eike Batista had a net worth of $35 billion and was hell bent in becoming the richest man in the world. By 2014 he was worth nothing, less than nothing.

This clip is from July 2013. Worth it!

Eike was overly aggressive. In the business risks that he took and the balance sheet (and funding practices) that he and his businesses operated with. A few project delays and a bad market was enough to cause a debt squeeze which ended up bankrupting him (and resulted in him ending up in jail for corruption). Eike was just too fragile.

And a headline from 2019:

Brazilian businessman Eike Batista has been found guilty of market manipulation and sentenced to eight years and seven months in prison.

Is Elon Musk flying too close to the sun?

Tesla shares are currently selling for ~20 times Sales (was at 3X pre-covid) and have a total market cap of $1 trillion dollars. This has Elon valued at >$250 billion personally, making him the richest man in the world.

Elon’s grand success has allowed him to monetise ~$17 billion (gross of taxes) of stock market value by selling shares in his companies (overwhelmingly Tesla).

This big share sale came after Elon asked Twitter in a late-2021 poll whether to sell 10% of his stake in Tesla. Elon always finds a way to mask his *actual* intentions with more ethical motives... 🤦🏻♂️

The case of Elon Musk and Tesla is not the same as Eike’s. Elon didn’t use massive debt loads to fund Tesla’s operations. But his personality cult allowed him to engage in capital increases via equity raises to fund his projects.

Tesla going well..or just better than before.

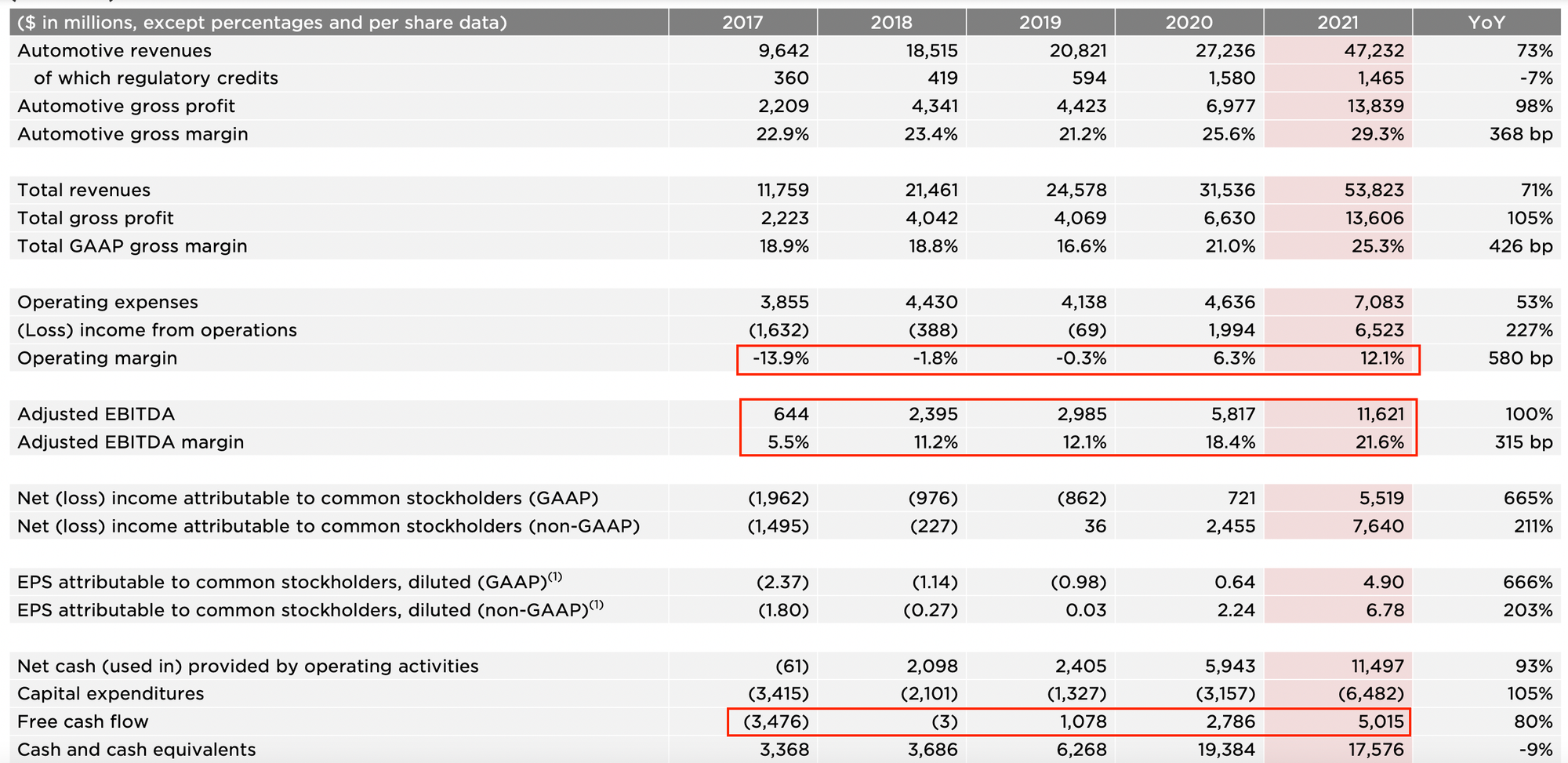

2021 was a blowout year for Tesla.

Cars produced and sold nearly doubled year on year. They are finally cash flow positive (even after deducting carbon credits).

Things look good for the time being. But competition is increasing. Executives are departing in droves and that never bodes well. Shareholder lawsuits and SEC investigations could become more material. Serious problems could come at any point.

But even if Tesla continues selling 1 or even 2 million cars a year, is that sufficient to maintain a $1 trillion market capitalisation? As mentioned above, shares are selling for a Price to Sales of 20 times. Jim Chanos insists that Tesla is an auto company. Not a technology company with wild margins and wild growth that could even slightly support such price multiples.

So what will happen if Tesla shares fall back to earth, even just a little? 🤏

This is what Chanos had to say on CNBC 4 years ago:

“The only two companies with an executive departure list like this was Valeant and Enron.…And so both of those were led by cult-like leaders who had changed the paradigm in their industries., Valeant in pharmaceuticals and Enron in Energy.”

…“I think Mr. Musk has crossed the rubicon in terms of making statements to investors that he might regret later….”

Elon buys Twitter

After a bit of a tussle, the Twitter BoD has accepted Elon’s offer to buyout the company for $54.20 / share. That’s $43 billion that Elon definitely does not have.

There has been talk of financing…and one could reasonably expect that Tesla shares would be posted as collateral for that debt financing to go through.

Elon’s back of the envelope DEMISE…

OK so how could this deal be financed? Assume Elon puts down $10 billion, and borrows $33 billion to get the $43 billion required for the buyout. Assuming a 5% interest expense on the debt, Elon must find a way to shell out another $1.65 billion per year in interest payments. Not to mention principal repayments.

The thing is Twitter doesn’t really make any money so he won’t be able to generate those instalments from Twitter. In fact, Twitter’s cash expenses are expected to increase as it will no longer be a public company and be able to issue share-based compensation to its staff. And those guys are spoiled…

Share-based compensation is ~$500 million per year, since 2013. Where is all that going to come from now?

Actually, I wonder if the guys from Twitter accepted Elon’s offer to cash out and subsequently bail on him and the company (it’s a possibility).

In any case, if Twitter doesn’t start generating cash fast and Tesla shares sell of from 20 times sales to even 10 times sales. Elon could go bankrupt.

As Tesla noted in its third-quarter Securities and Exchange Commission 10-Q filing this year: “If the price of our common stock were to decline substantially, Mr. Musk may be forced by one or more of the banking institutions to sell shares of Tesla common stock to satisfy his loan obligations if he could not do so through other means. Any such sales could cause the price of our common stock to decline further.”