Rufus: The first-level thinker

The story of Rufus the first-level thinker who got his levels confused and played the wrong game.

This is another Philosophy & Mindset piece, written to be timeless and to serve both retail and professional investors alike. This is the third piece in the Rufus series. Rufus is the typical anti-investor and he makes all the mistakes in the book.

Short-term price movements represent the market’s (biased and always by trial and error) attempt to value securities. In this domain, markets move like rubber bands pricing in the worry of the time.

Investors try to price in wars, pandemics, fed moves, inflation, disinflation, growth and all sorts of future macro and company-specific developments.

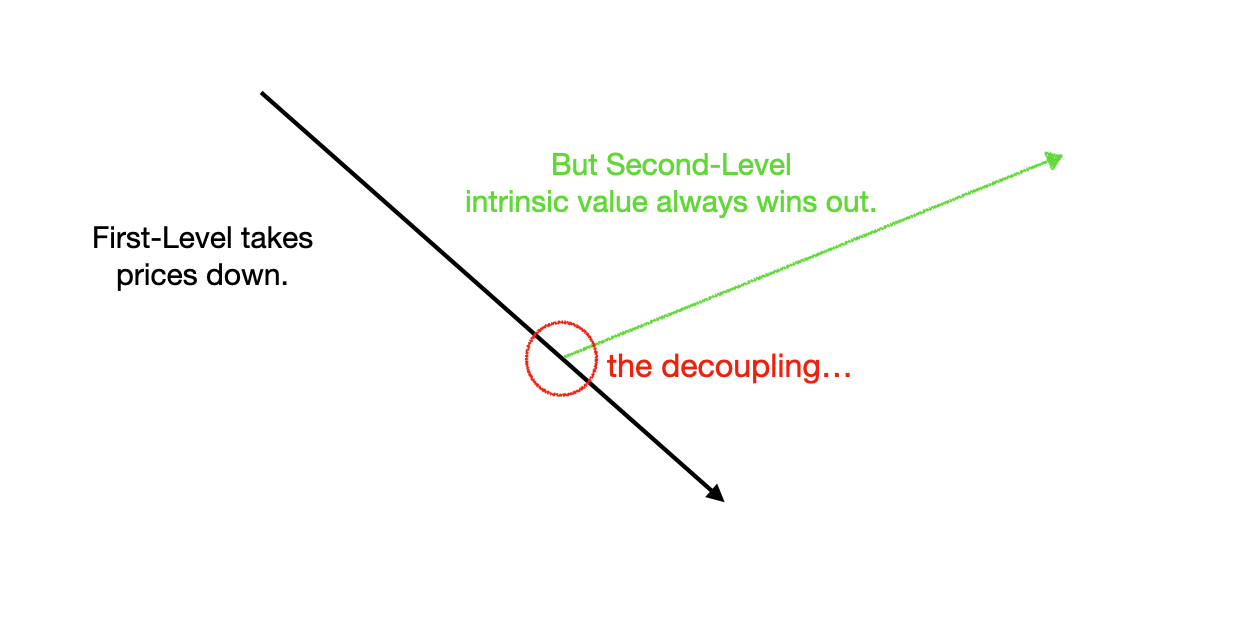

They apply their views of what is happening and their expectations of what will happen - and that is what markets reflect. Eventually, the extrapolation of this first-level thinking takes prices to a point which gives rise to a predictive fallacy.

This happens when the first and second levels decouple. That is, the market drops in an attempt to price in a negative expectation but prices move further than what is reasonably expected if that negative expectation were to be completely discounted (i.e. prices have undershooted).

In the second-level domain, investors take a longer term view of each security and try to value it using numbers, facts and business realities. This is also known as intrinsic value and over the long term, prices tend towards that value.

The implication of this is that there is no point in betting on events even if your prediction becomes reality. The reason is simple. You are not directly betting on an event happening, you are investing by paying a specific price for a specific asset which is only partially affected by the event occurring or not.

And these are two completely different things. (Exceptions exist. Like clinical approvals gone wrong and near total loss type outcomes etc.)

Let’s see how Rufus got it wrong…and a better way to go about things…

Rufus picks the wrong battle

“There are problems brewing - now is not the time to be holding stocks. Inflation is spiking and the Fed will taper. Things will crash…”

One month later Rufus goes back to meet his friends. They don’t start talking about markets but he can’t help himself. “See? I told you so!”

“Your stocks are down 20% since last time we spoke! And the war hasn’t even started, the Fed hasn’t even started to taper, [insert any negative event], etc.”

Ignorant investors still holding their stocks are about to experience a pain like never before. SELL!!”

In fact, that is how many investors feel; hence the sell-offs & volatility. And Rufus feels vindicated. Volatility continues but some stocks haven’t really registered new lows. But sentiment is still in the doldrums.

Rufus is certain the events he mentioned will cause a recession and bear market for years to come. He is certain he is going to buy everything up dead cheap! Meanwhile, he doesn’t know what he wants to buy, he hasn’t studied any companies, he is not prepared.

I think all Rufus wants is for prices to crash to the levels he should have bought but is still beating himself that he didn’t. I think he wants everyone to bow down to his oracle-like predictive powers.

His emotions are getting the better of him. While the market is having a hard time, he is feeling euphoric and elated.

He is forgetting all the previous times he had the cash to invest in good companies at low valuations, but he didn’t. He doesn’t care because “this time is different.”

But seemingly out of nowhere, the second level stages an offensive and the first level is forced to retreat.

After the sell-off, astute and prepared investors are seeing opportunities. There are some really good businesses selling for low valuations, some even too low. They are focusing on individual stocks and their long-term intrinsic values - not worried about the recent problems everyone else is focused on.

Markets have digested [insert worry of the time] and unreasonable fears have started to subside. They have accepted that the Fed must taper and rates can’t be near-zero forever. Inflation spiked but has since faded - even though it is still there.

Companies have started to increase prices to adjust to rising cost price inflation and their quarterlies are starting to look better. Under the spell of the first level, good results were a reason to dump. Now they are a reason to buy with both hands.

Markets are starting to believe in the long-term again. Their calculations are telling them that price-to-value here is indicating that forward returns will be high.

Rufus and his group of first-level friends are calling this a bear market rally. They are convinced that markets have entered a bear market and will drop much more.

The why? I don’t know. But there is nothing that can convince them to buy and hold good companies for the longer term.

The small bounce is turning into a broader market rally.

Rufus is pulling up old rallies that ended up selling off to new lows and layering them on top of the current market cycle.

He knows this has happened before and damn it he is going to find it! He finds a similar cycle and layers it on top - he’s got a match! He feels so pleased about his analytical prowess and superior judgment.

The elation from being right in first-level world was so high there is no way he is losing that. This rally? Rufus will not be buying. Besides, it’s already 20% to 30% higher from the lows; why buy here?

The thing is, Rufus can’t understand that your goal as an investor is not to predict short-term market moves. Your objective is to value businesses and buy them at a discount from their intrinsic values.

Rufus is playing the wrong game.

There is a better way

The long-term investor has to balance the first level with the second level to get the best results. The best analogy for this is the parimutuel betting system.

Basically, if you bet on a good company which is priced as a good company, you won’t make much because you just get what you pay for.

But if you use a short-term price drop to make a long-term investment on a good company, you stand to make a lot of money. It’s all relative.

And this is why, paradoxically, when things look bad you have to look for opportunities and when things look good you have to wonder if your investments are priced for long-term outperformance or destined for below average results.

“So you can get very remarkable investment results if you think more like a winning pari-mutuel player. Just think of it as a heavy odds against game full of craziness with an occasional mispriced something or other..”

— Charlie Munger

APPENDIX

The First and Second Level Decoupling

For the avoidance of all doubt:

First-level thinking is simplistic and superficial, and just about everyone can do it.

Second-level thinking is a more nuanced, long-term way of thinking which finds ways to gain an advantage over the first level.

Previous examples of first and second-level decoupling:

1) When markets crashed in early 2020 because of covid. Why “decoupling” ? Because in many instances first-level thinking took prices to such a low level that even with covid for years, intrinsic values wouldn’t go that low.

2) A little more than a year after the 2020 bottom when stay-at-home stonks rallied to such heights that even if we stayed home for 3 years straight they wouldn’t be worth that much.

The point is; neither one of these expectations was off the mark, but in both instances those who blindly jumped on that bandwagon lost their shirts. That is to say, those who sold the covid bottom and those who bought the stay-at-home rally.

There is a better way.

Further Reading

Philoinvestor: An Autointerview

Why you want stocks to go down

Investing is an endless poker game

Sketching it out