Why I don't like Transocean.

A pre-bankruptcy offshore driller.

In late 2021, I wrote about Valaris - the result of the merger between Ensco and Rowan. Ensco had already acquired Atwood Oceanics in 2017 — so the combined Valaris is made up of Ensco, Rowan and Atwood.

Severely hurt from the 2014-2015 oil price bust, the offshore drilling sector was dealt a final blow when Covid-19 struck in early 2020. In August 2020, Valaris filed for bankruptcy, but after its restructuring now operates with a net cash position.

Seadrill filed for bankruptcy in 2017 and then again in 2021, before emerging from its restructuring in early 2022. Seadrill later acquired Aquadrill (formerly Seadrill Partners).

Seadrill is also running with net cash balances and waiting for higher day rates on its rigs. But there’s an offshore driller which never actually filed for bankruptcy like the rest.

Enter Transocean, a pre-bankruptcy offshore driller

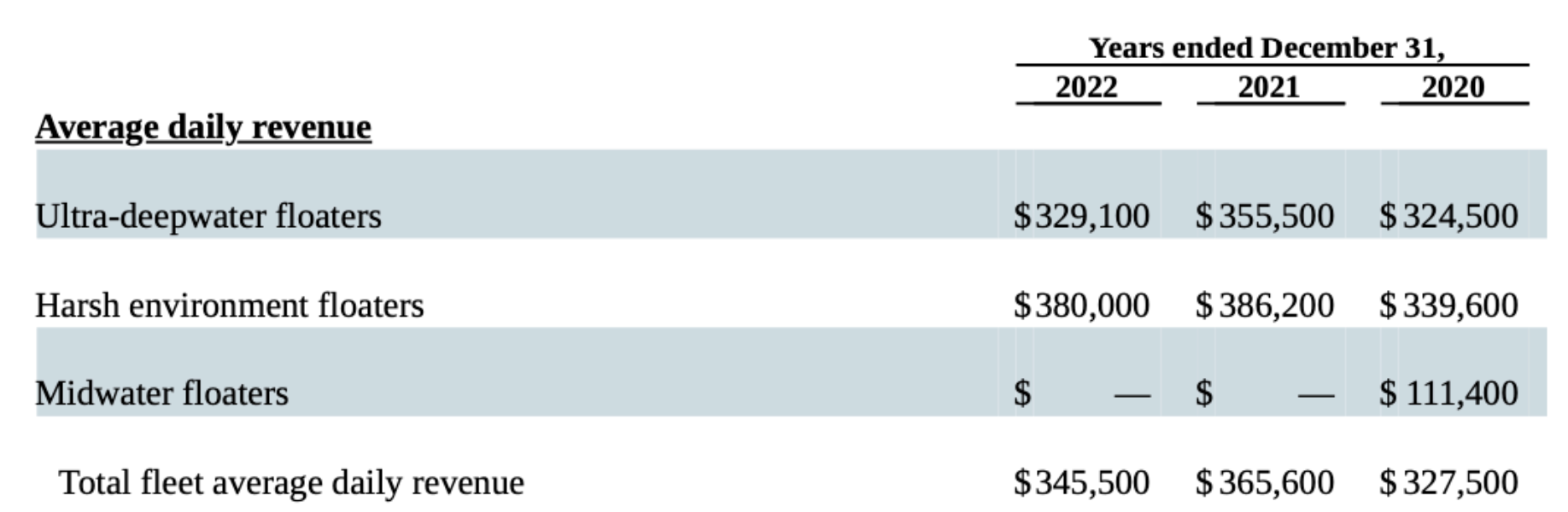

Transocean carries by far the biggest fleet of floaters (drillships, submersibles) but also the heaviest debt load. For the last 3 years they paid ~500 mln USD in annual interest expense or 20% of revenue (16% of 2023E revenue). Net debt y/e 2022 stood at $7.3 bln, equity at $10.7 bln while market capitalisation is now at $4.7 bln.

Total rig utilisation for the Transocean fleet is running very low. These assets are extremely expensive, the debt is very costly, and preservation stacking also costs millions every year. This isn’t an easy business.

In 2018, Transocean acquired Ocean Rig (a George Economou venture), for $2.75 bln in a cash and stock deal. It wasn’t a great move…Total rig utilisation for the sector continued to fade since then and those rigs are locked up off a Greek island somewhere rotting away.

Out of the 10 rigs that were acquired in the deal:

- one was placed in a venture that will focus in deep-sea mining

- two have been cancelled before delivery

- two are employed in Brazil

- one is employed in Angola

- one is employed in the US Gulf

- and three are stacked

Overall is the trade in the money? Doubtful.

Transocean total fleet utilisation is low, day rates are mid-cycle and money is getting more expensive. Transocean has executed on a number of “liability management transactions” to extend maturities and preserve liquidity until the cycle turns.

The bull thesis and reasoning around Transocean and offshore in general is simple. The idea is that global crude demand is increasing year by year, and that offshore drillers are required to achieve that. After the bust post-2014, the high cost to build rigs and the lack of capital in the sector means a building cycle is not expected any time soon. But so what? That’s just first-level thinking, scratch the surface.

At peak-cycle drillers make ~40% in EBITDA margins and only barely breakeven in low-cycle territory.

So in a low or mid-cycle the interest expense, the overheads, the wear and tear and the drop in asset valuation could wipe you out. Therefore ultimately, owning the equity stack in this business is not the same as outright buying the rigs on the cheap.

It is more like being long an out of the money call option on day rates, but with serious time decay. Bulls believe they are holding an asymmetric options on offshore drillers - but positive asymmetry means you have more upside than downside.

Bulls believe they own a ticket to spiking day rates and that they stand to make a killing when that happens. Furthermore, they believe that oil & gas companies are forced buyers of their rigs and so day rates will inevitably double from here…

Transocean is also fully concentrated to the most volatile subsegment of offshore - floaters. Other companies like Valaris have a large share of their rigs in Jackups which have less volatile day rates. This resilience can shield an offshore driller in tough times.

In the case of Transocean shares that is not the case. The idea of the option and the concept of optionality is about more upside than downside. But is this case with Transocean?

ATM (at-the market) Equity Offering

After the Covid downturn, management realised equity was slim relative to the assets they were carrying. In 2021 they issued 61 mln new shares for $263 mln and in 2022 another 36.1 mln for $158 million. That’s ~97 mln new shares for $4.35 per share, from a total of 595 million before the issuance (a 16% increase).

Book Value for y/e 2021 and 2022 stood at 11.2 bln and 10.8 bln — while ATM equity offerings were filled at prices ~70% lower than that.

The Newbuilds

The biggest capital outlay of the past two years are the two newbuilds that will soon be delivered to Transocean. The Deepwater Aquila and the Deepwater Titan are top of the line 8th generation drill ships with increased capacities for production. Titan’s sister ship Atlas was delivered last year, these 3 assets cost more than $1 billion each.

Their features allows exploration and development to go to sites and wells that were previously not feasible. These are great assets, but are they great for business?

Deepwater Atlas and its sister ship Titan were ordered back in 2014, and they're only being delivered now. Can you provide some color on the challenges faced since the original order? The rigs reportedly cost $2.25B in total, versus $1.08B when originally ordered.

the reply from Transocean’s Technical Marketing Manager👇

While the rigs were originally ordered in 2014 just before the industry downturn, these two projects shifted in 2018 when one of our customers approached us with an opportunity to design and construct a rig capable of drilling in 20,000 psi environments – the new frontier of ultra-deepwater drilling. As a result of the new rig design and construction management contract, and a five-year drilling contract, we shifted gears and got to work to accomplish the design, construction and delivery requirements set forth in the construction contract. The initial contract for the Deepwater Titan adds $830 million in backlog and the initial contract for the Deepwater Atlas adds $252 million in backlog to Transocean’s industry-leading $7.3 billion backlog as of October 13.

Excerpts above from Maritime Magazine article

The Titan, having cost $1.18 bln during 8 years of construction has won a 5-year contract for $830 million, or $454,000 per day. Assuming $150,000 expenses per day gives you ~$300,000 cash-flow before financing costs and depreciation.

Assuming 8% cost of debt and a 50% LTV (loan-to-value ratio) gets you $50 million a year in interest. Therefore, the back of the envelope economics of such an expensive drill ship (considering 365 operating days), are: $300,000 x 365 = $109.5mln in cash flow.

—> $109.5mln minus interest expense of ~$50mln = $59.5mln before depreciation…Considering a 30-year life for the drill ship (ignore scrap value for now) brings you to a ~$40mln depreciation expense per year. The economics are so abysmal I don’t need to move further into refinancing dynamics and allocation of G&A costs.

Turnaround or just posturing? 🙄

Transocean management is extremely vocal about a sustained recovery in offshore drilling, and that their high-quality assets (stacked or active) will benefit tremendously from this. At the same time however — they communicate things that I consider to be contradictory.

“We look to apply lessons learned from the delivery of our newbuilds as we reactivate our cold-stacked assets. A successful reactivation is not only completing the project work scope in line with cost and time expectations, but also starting operations safely, reliably, and efficiently. To achieve this, a drilling contractor must have a robust operational management system and culture…….We look forward to the opportunity to steadily bring back our idle fleet back into service in the safest, most cost-effective manner to best ensure the highest returns for our shareholders.”

“Having said that, we would absolutely firm our position that we will not reactivate our rig unless our customers, through a combination of mobilization fees, day rate, and term pay for the entire reactivation plus an acceptable return in the initial contract.”

“Brazil has been an important source of demand for the last two years, and we expect this to continue in 2023. Importantly, the incremental demand is driving higher day rates with an already 107% increase from 2020 to 2022. We anticipate that new fixtures will continue to climb as active supply in the region is exhausted, requiring assets from other regions, of which will need to be reactivated and upgraded to be mobilized to support the demand in Brazil.”

“I think we’ve been very clear in our position on reactivation that the customer has to pay for it in the first contract, and some form of upfront payment, mobilization fees, plus day rate and term that more than paid for the reactivation itself and actually generate the suitable return for Transocean. And so, that may mean that we’re later to do the reactivation party than some of our peers if they’re willing to reactivate on spec or for less of returns, and we are OK with that.”

“However, when we went through the details of this and we went through the timeline that Petrobras was going to execute upon, we decided that the cash flow just didn’t meet our return requirements. So we stepped aside from that one and took the disciplined approach of not putting forward the Athena into that tender. Petrobras moved to the next operator, and that’s going to be the DS-8, which should see their award at $460,000 a day….But we just want to reassure you that we take that discipline very, very seriously. And we have walked away from some contracts because they did not provide returns we assess to be adequate.”

“Look, the goal of the actions we’ve taken over the past 12 months was to buy ourselves some time.”

“But I think what we’re seeing right now is the first in line are not the cold-stacked rigs. It’s the rigs that have been completed that are sitting at the years in South Korea…We don’t believe that any of those rigs can really start on their contracts in 2023 given the fact that there’s a consensus around at least 12 months to reactivate a rig from the shipyard or from cold and to prepare the rig for its contracts…So I think it’s going to be measured mainly because of this constraint, but also because of the fact that there is a significant amount of cash required to do this. And if you look at the balance sheets of the drillers, especially those that have gone through a restructuring, I’m not sure it supports a wholesale reactivation program unless it’s paid upfront by the customers.”

Discipline or Moneyness?

Transocean is trying to communicate that the market is turning and that interest for offshore drillers is increasing, that they are looking forward to bring their stacked rigs out of preservation, that costs to reactivate are very high and that drillers don’t have that kind of cash lying around and that they take a very disciplined approach to reactivate their own rigs requiring that the customer pays all those costs and offer a suitable return for the company on top.

All this seems paradoxical to me for an overlevered company in a highly cyclical capital-intensive sector which admits they are trying to “buy some time” as the reason for their liability management exercises.

Is this why Transocean management is talking such a big game about the market and the rates they are willing to lease their rigs at? Is it because most if not all of their stacked rigs are actually never coming back to activation because of how badly they maintained them all those years? Could the market slowly realising this cause a repricing in its capital structure — making the company unable to finance its operations going forward?

So you see, I would take communication from management with a very heavy pinch of salt before making any serious assumptions about the opportunity here.

Forced Buyer or Forced Seller?

Transocean management and many vocal shareholders view oil companies as forced buyers of rigs because offshore is the only way to increase annual crude production etc.

But profitability of offshore drillers is the derivative of the derivative of oil barrels consumed — the relationship is never linear.

Conclusively, the level of capital expenditure needed to keep these assets operational, the cyclicality of utilization, day rates and hence profitability, the depreciation / wear & tear as well as the constant financing requirements and interest expense required to stay afloat makes the equity of Transocean like a way out of the money option with fast time decay.

You stand to make a killing in the chance that day rates move very far very fast and stay there, or stand to get killed if things move sideways from here.

Finally, while many talk about a sustained cyclical recovery in day rates and utilization — there are no guarantees that this is the case, rather, it could be a short upswing amidst an overall sideways market.

I expect Transocean to engage in further ATM equity offerings going forward, as it becomes clearer that the equity stack of their capital structure cannot sustain the assets they hold.

Alternatively, they could look to sell their 8th generation drill ships to fortify their balance sheet and deleverage. However, doing that would be very inconsistent with management rhetoric as well as reveal that no serious bidders would emerge for them without Transocean being forced to take massive losses on those assets.

I don’t think oil companies are forced buyers, I think Transocean is a forced seller of their assets. Thus, one should distinguish between return on capital and return of capital in cyclical, capital-intensive businesses.

Petrobras Plans 🛢️🇧🇷

It seems the offshore market is hanging by a Petrobras thread, waiting for the company to come out with a big tender for rigs and soak up supply pushing day rates to move up. But what if it doesn’t?

I don’t know what Petrobras will do going forward but a Brazilian investor 👇 casts doubt on further exploration that would be big enough to warrant massive chartering of offshore drills.

He believes Petrobras, under the new management of Jean-Paul Prates, will invest a lot of capex in “clean energy” like offshore wind as well as increasing their refinery capacity. He also believes massive Petrobras dividends are a thing of the past and will soon start to be cut as it becomes clear how much increased capex and opex Petrobras will make.

Reversal

The bull case could play out if oil moves up towards $100 and stays there for enough time to change oil company behaviour. For the moment the long end of the oil curve is at ~$50 — indicating that we are far from it.